I’ve long considered Thinking, Fast and Slow my favorite book on investing, not because it teaches forecasting, but because it clarifies how humans actually make decisions under uncertainty. At one point in the book, Daniel Kahneman suggests that if you are allowed one wish for your child, you should seriously consider wishing them optimism, not because it guarantees success, but because it fosters resilience, adaptability, and an orientation towards opportunity amid uncertainty. That perspective has taken on new resonance for me, as I recently became a father and the beginning of a new year ushers in “prediction season,” when market outlooks proliferate and the illusion of predictive certainty becomes most compelling.

The Real Risk Isn’t Being Wrong

Twenty-three years of industry experience have taught me that the real risk in investing isn’t prediction itself, but the belief that successful investing depends on it. A prediction-oriented mindset is appealing because it offers the illusion of control and clarity when the future feels knowable, even though it never is. However, when applied to investment strategy, it is usually counter-productive, not simply because predictions tend to be wrong, but because organizing decisions around them encourages reactive behavior, unnecessary activity, and abandonment of sound strategies at precisely the wrong moments. Informed optimism offers a more durable alternative. Grounded in evidence, it accepts uncertainty as a permanent feature of markets and enables the patience and discipline that has reliably led to long-term success. If there is one lesson I would want to pass on to my son, this would be it.

Why Market Forecasts Fail as a Decision Tool

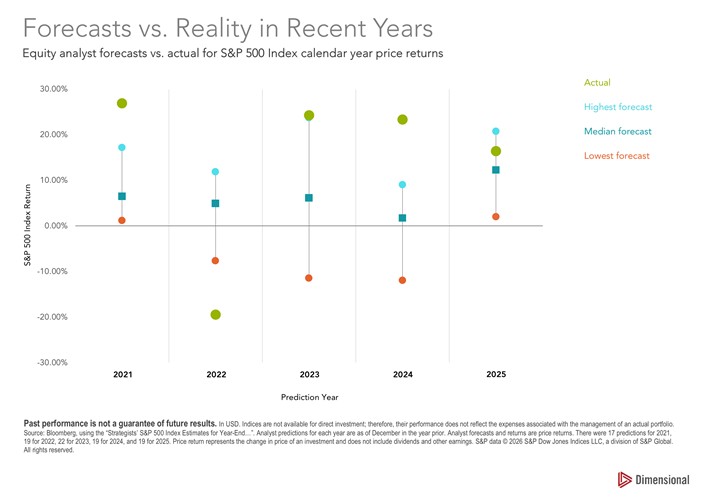

Each January, Wall Street produces a fresh set of confident market forecasts, and each year the results look strikingly similar. The Dimensional data makes this plain. Analyst forecasts for S&P 500 returns tend to cluster tightly around reasonable expectations, while actual outcomes routinely land far outside that range, sometimes much better, sometimes much worse, but rarely close to consensus. The takeaway isn’t that forecasters lack intelligence or effort, it’s that the exercise itself fails to provide reliable guidance. Year-ahead predictions consistently miss not just direction, but magnitude and volatility, the very dimensions that matter most for real-world investor decisions.¹

When forecasts cluster and outcomes diverge, the problem isn’t effort or intelligence—it’s relying on prediction as a decision-making tool.

Why Even “Right” Forecasts Often Don’t Help

But stopping there would miss the deeper point. As research by John Cochrane, a leading scholar of how markets price risk and uncertainty, makes clear, the problem with prediction runs beyond inaccuracy. Even when forecasts about expected returns or macro conditions are directionally correct, they are often still unhelpful for investors. Markets price expectations, not outcomes, and returns are driven by surprises relative to what is already known. Signals about expected returns are weak compared to day-to-day volatility, and exploiting them requires long horizons, precise timing, and behavioral endurance that few investors can sustain. In plain terms, even when smart forecasts are directionally right, turning them into better outcomes is far harder and far less reliable than it appears. In practice, organizing decisions around forecasts, even informed ones, tends to encourage the very behaviors that undermine outcomes: overconfidence, reactive shifts, unnecessary activity, and abandonment of sound strategies during inevitable rocky periods.²

Why Optimism Works When Headlines Don’t

This chart from Dimensional Fund Advisors tells a simple but easily forgotten story: markets have rewarded discipline far more consistently than they have rewarded articulate outlooks, persuasive narratives, or tactical forecasts.

Over more than five decades, investors have endured inflation shocks, recessions, wars, financial crises, pandemics, political turmoil, and a steady stream of headlines insisting that “this time is different.”

And yet, through each episode, long-term investors who stayed engaged were compensated, not because risks disappeared, but because progress continued despite them.

Maintaining discipline through decades of headlines has required optimism,not about the next market move, but about long-term progress.

This is where informed optimism becomes not just helpful, but essential. Without an optimistic mental filter, one anchored in durable, long-term progress and a robust, well-designed strategy, investors are constantly tempted to interpret new information as a signal to adjust, refine, or outguess that strategy. With it, the right behaviors become easier. Movements and forecasts are informational, not instructional. Optimism doesn’t dismiss headlines or deny risk; it places them in proper context so that patience, discipline, and staying invested remain achievable in real time. That’s the role TCI’s investment approach is designed to play: not to predict what comes next, but to help clients remain aligned with the long-term forces that have rewarded disciplined investors again and again—even when the temptation to forecast is strongest.

How TCI Embeds Informed Optimism in Practice

This is what value-creating optimism looks like in practice: not ignoring risk, but acknowledging it honestly while staying focused on the decisions that matter most. By centering portfolios on durable, long-term forces and a well-designed strategy, our approach shifts attention away from what can’t be reliably influenced and toward what can: diversification, discipline, and time. That focus reduces the impulse to intervene unnecessarily and makes it easier to live with the parts of investing that will never be fully controllable.

That’s the role TCI Wealth Advisors plays for clients: not to predict what comes next, but to help them remain aligned with a sound investment strategy and a healthier decision-making posture. In a world that constantly invites prediction, informed optimism provides a steadier foundation, one that supports better outcomes over time, and a more livable investment experience along the way.

Footnotes

¹ Dimensional Fund Advisors — Market Forecasts vs. Reality.

Analysis showing that year-ahead market forecasts cluster narrowly while realized outcomes vary widely, illustrating why forecasts fail as reliable inputs for investor decision-making.

² John Cochrane — Presidential Address: Discount Rates. Journal of Finance.

Examines how expected returns and discount rates are priced in markets and why even informed forecasts about expected returns are difficult to translate into actionable investment decisions.

TCI Wealth Advisors, Inc. is an SEC registered investment advisor. This material has been prepared for informational purposes only. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No client or prospective client should assume that any information contained herein serves as the receipt of, or a substitute for, personalized advice from TCI, or from any other investment professional. Please remember that different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy (including those undertaken or recommended by TCI), will be profitable or equal any historical performance level(s). No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if TCI is engaged, or continues to be engaged, to provide investment advisory services.